Eliminating debt is the first step you need to take to achieve true financial freedom. Did you know that 87% of lottery winners become poor again within 24 months? In fact, you might be surprised to learn that they become poorer than before in less than two years because they are overwhelmed by debt.

This statistic shows us how crucial wise money management is.

I believe that if there were a great reset tomorrow and all the world’s wealth were evenly distributed, within a generation we would return to the starting point, with rich and poor people. But if we can’t even stay rich after winning the lottery, I wonder, how can we manage money effectively?

This skill isn’t taught in schools, and that’s part of why I’m writing my personal finance blog, to spread knowledge about financial education.

Cognitive Biases about Money

Our biggest enemy in managing money is ourselves, with our cognitive biases.

The topic of biases is extremely important, and I am preparing a series of in-depth articles on it. This English term refers to prejudices or cognitive distortions that influence the way people make decisions and judge situations.

The first thing you need to work on if you want to manage your economic resources better is to try to avoid mental accounting bias (mental accounting), which alters our relationship with money. Your brain assigns different values to money; for “it,” one euro is not always worth one euro, but its value depends on its use or origin. For example, if you receive a bonus at the end of the year, it is very likely that you will use that money differently than you would your regular monthly salary.

My Money Management Method

At this point, I think it’s time to introduce you to “my” method of money management, which I have developed over the years.

Personal finance, being personal, does not have rigid rules but can be interpreted differently by each of us, as described by the parable of the six blind men and the elephant. In my case, it is important to note that I was an executive with a fixed monthly salary. This aspect probably made things easier for me compared to those who do not have the fortune of regular income throughout the year.

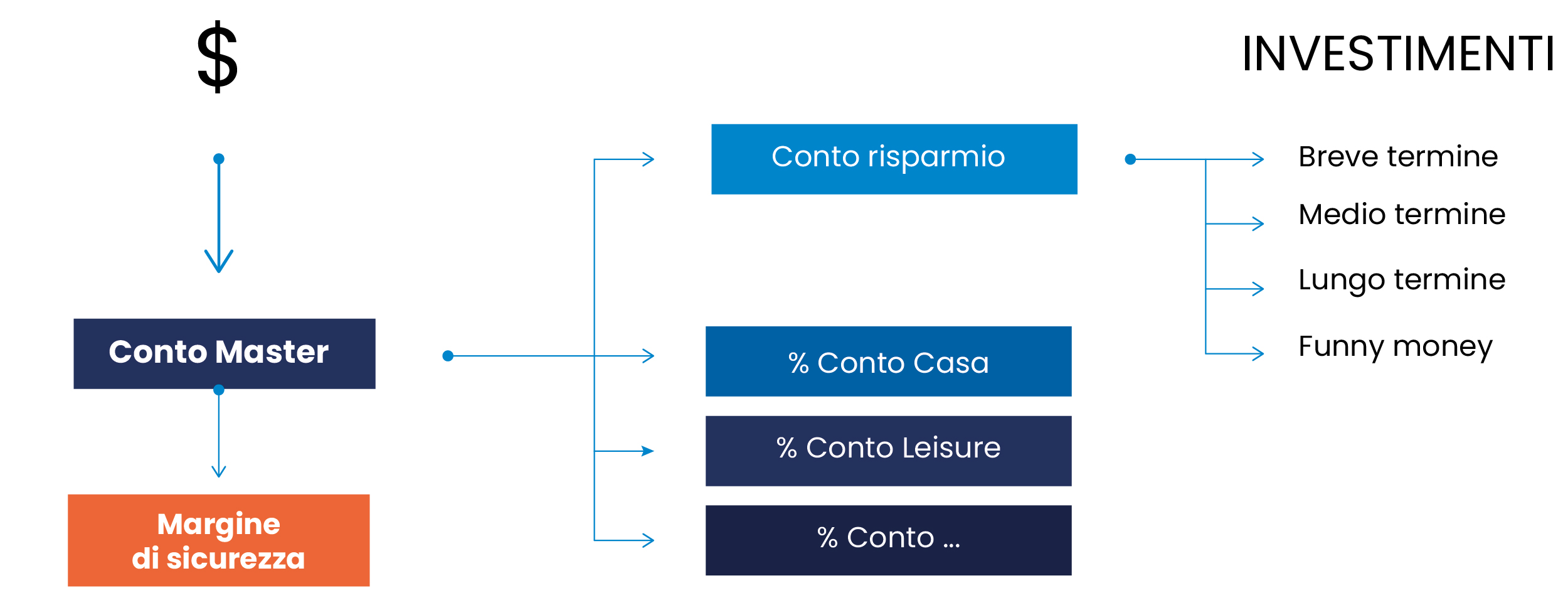

First of all, I recommend having multiple bank accounts which you should fund automatically based on prior financial planning and your personal budget. Tracking your income and expenses, and having reliable numbers, is a necessary exercise if you want to manage money properly.

Before implementing the system, two preparatory steps are needed.

The financial map for money management.

First Step: Quantify Your Debt Position and Take Action

By debt position, I mean the total value of your debts excluding any mortgage on your house. You need to determine all your other debts, such as consumer credit loans, car loans, smartphone installments, revolving credit cards, etc. The reason is simple: the interest rate or APR will likely be in double digits. Consequently, it will probably be higher than the interest rate you can earn from your investments. If you look at the problem from a different perspective, you are already investing, not in stock markets, but at an excellent rate of return.

The first goal is to gradually eliminate all debts to become “Debt Free.” It will probably take several years. My advice is to start with the smallest debts and work your way up to the larger ones; you need to trigger the “snowball effect.”

If you have too many consumer-related debts, for example, if your car costs over 30% of your income, you should sell it and buy a smaller used car. You could even choose to go without a car for a few months and look for alternative mobility solutions. A small sacrifice to eliminate debt is easily manageable with some practical daily life organization.

Don’t worry about what your neighbors might think: you’ll find that these short-term sacrifices to eliminate debt will be more than compensated in the long run.

This will be a significant milestone that will give you incredible mental strength. I achieved this result in 2021, and since then my life has changed.

Your savings will be invested to eliminate debt

This task can be carried out monthly, but with a previously planned goal that must be achieved. The time required will naturally depend on the amount of existing debt. This is already a great investment!

Bad Debt versus Good Debt

A brief note on the topic of debt. What we’ve discussed so far is bad debt, which costs you more than you can earn from your investments and is generally used to purchase consumer goods. Eliminating debt also means knowing which ones to tackle first.

There is also good debt, which costs less than the returns from your investments and is incurred for investment purposes, not consumption.

A mortgage on a house is a hybrid and borderline form of debt between good and bad. Although it is contracted for a consumer good (albeit a primary one), if it allows you to reduce the cost you would otherwise incur for the house or if, in general, it costs less compared to the returns from your investments, then it can be considered good debt.

As you advance with your financial education, you will discover various forms of good debt that can help enhance your earnings. Some examples are margin loans provided by brokers to top investors on their trading accounts.

Remember, even in this case, it is still debt, so leverage should be used with caution. That’s why I told you it’s better to “discover” and use them when your financial education is at a high level.

You must learn to distinguish between bad debt and good debt. While the former costs you more than you can earn from investments, the latter can be an opportunity to increase your earnings. Prudent money management is essential for ensuring financial stability and freedom. Eliminating debt and understanding its different forms are the first steps towards financial freedom.

In the next article, we will analyze the second step: you will start to build the emergency fund which will later become your “margin of safety” (MoS).

On avance!