Throughout life, all of us will face problems with our car or home. However, this does not necessarily have to generate additional stress. In this article, we’ll explore how to manage emergencies correctly. You might be surprised by the solution.

The first step to achieving sustainable financial management over the long term is to become, over time, “debt-free“. This milestone will have a tremendous impact on your life.

What is an Emergency Fund

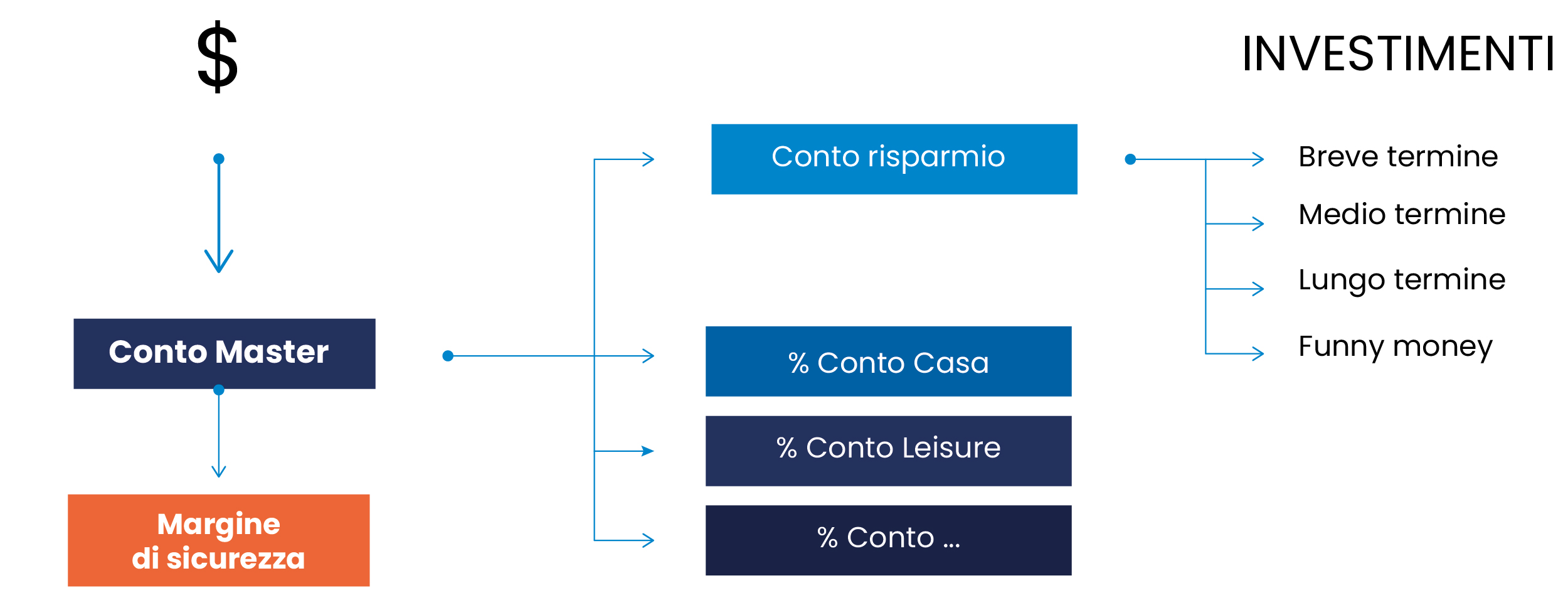

Now it’s time to address the second action: creating an Emergency Fund, which will later become your Margin of Safety (MOS).

Often overlooked, this fund plays a strategic role in ensuring financial stability and growth.

Your emergency fund should consist of at least one thousand euros in cash. Again, it’s important to take actions that provide you with peace of mind and security.

Start with small steps to reach goals that might initially seem unattainable, using the “snowball effect”. If you don’t have a thousand euros immediately, start saving monthly, but do it as soon as possible.

You should build the fund in the shortest time possible, keeping the money in a place that is easily accessible but not too visible. It’s also important to clearly define, preferably in writing, what constitutes an emergency and when you are authorized to withdraw funds. Again, you’ll need to fight against your brain’s biases that will categorize everything as an emergency.

Defining an Emergency Situation

In my opinion, an emergency should have at least two main characteristics: it must be unexpected and urgent. Some examples might help clarify the distinction. A sudden problem with your car, like a battery failure, is an emergency, but paying for insurance or filling up with gas is not.

It’s crucial to be aware that our brains tend to interpret any situation as an emergency. We live in an unpredictable world, and we should prepare to face the unexpected. Creating an emergency fund is like building a protective cushion to handle the unforeseen events life throws at us.

Preparing to Invest

When you’re ready to start investing in the stock market, I recommend following the buy & hold strategy and never interrupting it. This way, you can maximize the power of compound interest.

The Buy & Hold strategy is a long-term investment approach that involves purchasing financial assets, in my case ETFs, and holding them in your portfolio for an extended period. I bought my first MSCI World ETF in 2018 at 42 euros, haven’t sold it, and have no intention of doing so.

I believe that in the long run, the global economy and financial markets will grow, leading to a natural increase in the value of assets. If you want to be this kind of investor, you need to ignore daily market fluctuations and avoid selling your investments in response to short-term events, such as price drops. It’s not easy; it takes years, a lot of study, and a bit of personal predisposition.

I vividly remember the panic that gripped financial markets during Covid in March 2020. For me, this crisis turned into an unprecedented opportunity. In the end, the economic impact of the pandemic followed a U-shaped curve.

A brief digression for those who haven’t studied economics. You should know that financial markets can experience three types of trends during a crisis and the subsequent recovery: V-shaped, U-shaped, or L-shaped. However, no one can predict with certainty which shape it will take and how long it will last. For example, the 2008 financial crisis followed a U shape, while the crisis in Japan in 1986 was more L-shaped. None of us have a crystal ball to foresee the future.

How to Calculate the Margin of Safety

To create your MOS account, calculate all fixed costs (e.g., rent, utilities, etc.) and multiply them by at least 6. This number represents the months needed to find a new job, though there’s no precise rule. If you want to be more cautious, you can use 12 months as a parameter. If, however, you work in a “hot” sector and/or are in a more dynamic job market, you can be more aggressive and use 3 months as the multiplier.

Again, as often happens in personal finance, there’s no precise rule on how large your margin of safety should be, but I stress that it’s essential to establish it with some common sense based on your lifestyle.

I clearly remember when, in December 2021, I suddenly lost my job along with other colleagues due to a turbulent generational transition. Initially, this event caused me some disorientation, as is natural, but after the initial shock, having the margin of safety and zero debts meant that my life wasn’t turned upside down. I stayed in the same house, had time to get back in shape, and prepared for new challenges without having to interrupt my investments. On the other hand, other colleagues who lacked financial stability faced numerous problems. In the end, I emerged stronger and more prepared for new challenges.

Start Building Your Emergency Fund Now

Creating the emergency fund, which will become the Margin of Safety, is a crucial step for ensuring stability and financial growth over the long term. This fund, initially consisting of at least one thousand euros in cash, provides a safety net for dealing with unexpected events such as car or home issues, avoiding additional stress in daily life.

My personal experience underscores the importance of having a solid MOS. Even in the face of unforeseen events like job loss, a well-structured MOS allowed me to handle the situation with determination, without compromising my financial path by making significant withdrawals.

On avance!