Investing in Yourself as part of a financial strategy—really? The question that many people often ask me is: what is the best financial investment? Perhaps the answer might surprise you.

When it comes to personal finance, the focus is often immediately on the financial investments needed to achieve economic independence and how to eliminate debt. However, in my opinion, approaching the topic from this perspective is like building a house starting from the roof.

What I would like to try to do in my blog, “The Finance Club,” is help you build your house from the foundation and make it as earthquake-resistant as possible. The goal is to withstand the financial earthquakes that will cyclically hit it. It will be necessary to make sacrifices for a limited period, but this will allow you to radically change the course of your life.

Returning to the initial question, technically, the correct answer should be: the best investment is the one that generates the highest return. However, it is important to consider that the higher the expected return, the greater the volatility. To reduce risk, it is necessary to diversify and not put all your eggs in one basket. I could go on indefinitely with other phrases and examples, but for me, the answer is much simpler: the best investment is investing in yourself, so the best investment is you.

An investment in knowledge pays the best interest

Benjamin Franklin

What It Means to Invest in Yourself

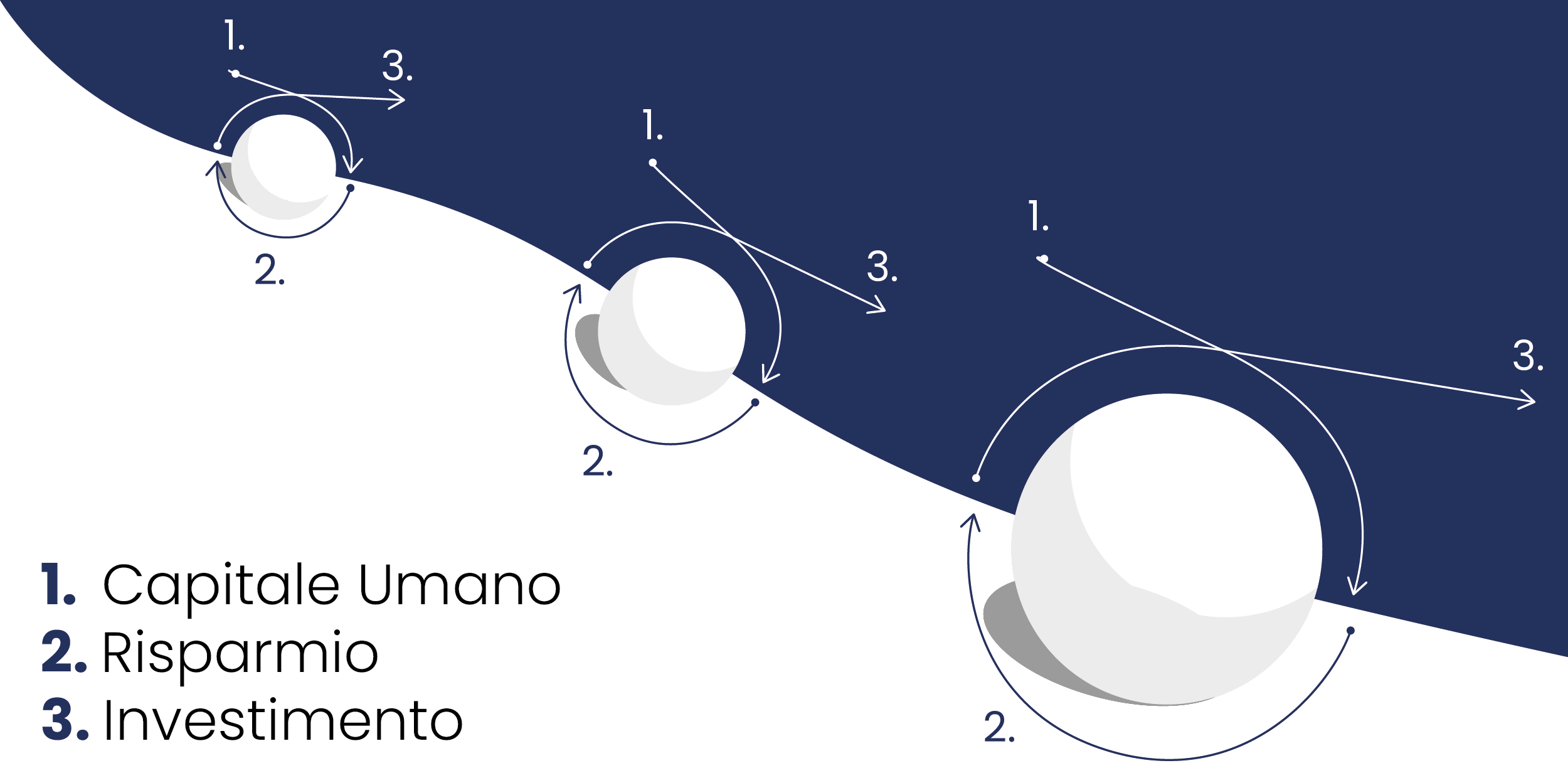

Investing in yourself means investing in education, training, skills, and relationships. All this aims to strengthen what we could summarize as our human capital, which will generate exponential growth in the long term and consequently help achieve personal and professional life goals.

The three stages to achieve financial independence.

The topic of personal growth is extremely complex, very fascinating, and certainly not something that a blog alone can cover exhaustively. Therefore, I will limit myself, based on my personal experience, to illustrating my reference model based on:

I will share some advice, especially aimed at avoiding serious mistakes.

Throughout our lives, we are constantly required to make choices. Some are irreversible, while others require a very high price to be changed. My philosophy, based on common sense, tells me that it is more advantageous to have the odds in your favor.

Education and training are the foundations on which you must build your success; in this field, you should never compromise

Avoid mediocrity and always seek excellence, pursuing your passions, because you have immense potential to develop.

At first, this process of seeking excellence may seem very costly and exhausting. This is because the human brain is not designed to handle calculations that at first glance may seem intangible and need to be analyzed with a long-term investment perspective using compound interest. We have a clear problem with “linearity” in decision-making. In some contexts, it would be appropriate to reason in a non-linear manner.

Linear and Non-Linear Decisions

Let me clarify with an example. In finance, a linear decision can be found in fixed-income investments. If you invest a fixed amount of money in a savings account that offers a fixed interest rate, the return you earn will be proportional to the amount of money invested. This is an example of linearity because the return directly follows the increase in investment.

On the other hand, risk management in finance and investment decisions can be highly non-linear, especially in volatile markets. For example, small changes in market conditions can lead to large changes in the prices of options, due to the exponential nature of their value relative to the underlying asset price.

These examples show how linear and non-linear decisions can vary significantly depending on the context and environment in which they are made. Understanding the nature of the relationship between variables is crucial for making effective decisions and predicting outcomes.

In modern society, most decisions we make do not produce immediate effects. If we save today, we might have a pension in a few decades. We live in what scholars call a “delayed return environment” because we must work for years before our actions yield the desired result. Conversely, our brains have evolved to prefer quick results over long-term ones. Behavioral economists call this tendency “temporal incoherence”, meaning that the way our brain estimates rewards is inconsistent over time. We attribute greater value to the present compared to the future.

Understanding the difference between linear and non-linear decisions is fundamental in numerous fields, from physics to economics, from business management to personal planning

The Flexible Approach to Decisions

Linear decisions, characterized by proportional and predictable relationships between causes and effects, offer clarity that can simplify planning and forecasting. On the other hand, non-linear decisions, with their complex interdependencies and unpredictable dynamics, represent a greater challenge but also an opportunity to use more sophisticated models and strategies to gain competitive advantages or better adapt to changing conditions.

In the real world, decisions are rarely purely linear or non-linear; rather, they often exist as combinations of both, requiring a deep understanding and careful analysis to navigate effectively through challenges and opportunities. Through examining the illustrated examples, it becomes clear that success in managing such decisions relies on the ability to recognize patterns and apply the right balance of analytical techniques and intuition.

Ultimately, whether it involves managing financial investments or simply planning your career, the approach to decision-making must be flexible. The ability to distinguish between linearity and non-linearity can thus provide a valuable tool for wisely navigating the complex landscape of everyday choices.

Investing in Yourself is the Most Productive Choice

The most productive investment you can make initially is not found in financial markets, but in yourself.

The concept of human capital teaches us that educating and training our mind and skills can lead to long-term benefits that far exceed the returns from financial markets. Decisions to invest in yourself may seem costly and demanding at first, but it is essential to recognize that this is an investment with high returns on our quality of life.

While modern society often rewards immediate results, true wisdom lies in appreciating and pursuing long-term rewards. This requires a non-linear perspective on life decisions, as the true value of our actions today may only manifest in the future. Temporal incoherence, a significant challenge in our reasoning, requires a shift in perspective to properly evaluate the present and the future.

The first step is undoubtedly to focus on increasing your income because it is the most powerful lever you have at your disposal. Stay away from those who promise to make you rich quickly and effortlessly.

In upcoming articles, we will further explore how choices related to Human Capital influence not only our financial path but also our personal and professional development.

On avance!