Numbers never lie, except when it comes to creating a personal budget! After learning how to track your expenses, you now have all the data you need to create your personal budget.

It’s very useful to make an accurate forecast, but it’s just as important to commit fully to sticking to it.

The Data for Calculating a Personal Budget

To do this correctly, I recommend starting with your Actual data, which should be processed to prepare both the personal budget for the current year and the forecasts for future years. Numbers are essential and rarely lie. Knowing your annual expenses is important in both the short and long term for setting and achieving your goals.

You’ve probably heard about financial independence and FIRE (Financial Indipendence Retire Early), as these are common topics both online and on this blog.

Do you have an idea of how many years it will take or how close you are to your goal of becoming financially independent? To do this in an informed way, you must start with your expenses and have reliable data.

For example, if over the past three years, you’ve spent an average of $40,000 per year, using the 4% rule, you’ll need around one million euros ($40,000 / 4%) to be financially independent. We will cover this topic in more depth in the Investments section, but for now, it’s enough to grasp the concept.

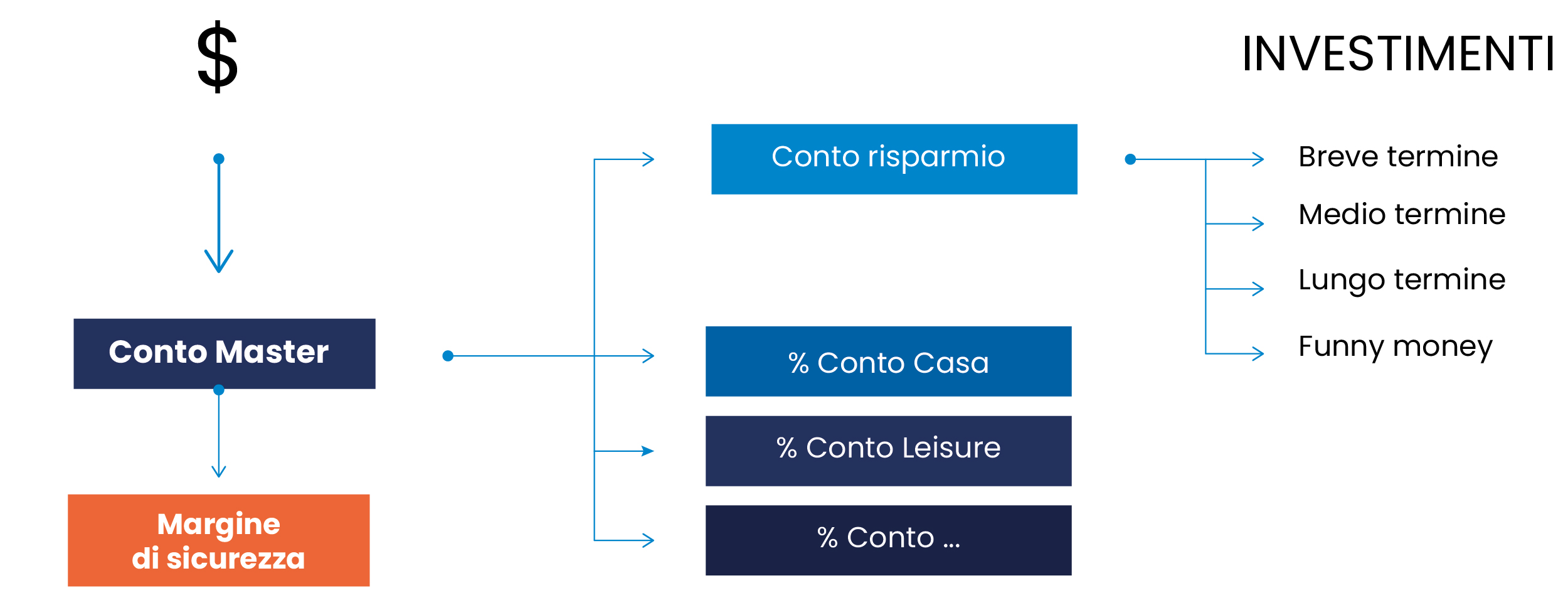

The same goes for the Safety Margin, which should cover at least six months of costs, so it should be at least €20,000.

The Goal of Planning

If you were driving your car without looking at the dashboard, it’s very likely you’d never reach your destination. The indicators provide us with the direction to follow, showing how far we’ve traveled, whether we’re consuming too much fuel, and so on.

The goal of the personal budget is to have a tool that helps you reduce current expenses by implementing a series of actions on the main expense categories in order to define a realistic savings target. You’ll have to work hard because it’s easy to get results on a spreadsheet compared to the real world. The results should be analyzed periodically and compared to the Actual data. The objective is to understand what went wrong and what went right. Finally, you’ll need to prepare a new personal budget for the following year—it’s a virtuous cycle that you’ll recalibrate every year.

The most important thing is to set a savings rate upfront, for example, 30%, and always account for a margin of error.

It’s crucial that this amount is automated through a periodic transfer and sent to a dedicated account on the same day your salary is deposited. I’ve been using Interactive Brokers (IB) for many years to perform this task.

Savings are the payment for the work you do, so you must pay yourself first

This is the correct mindset for managing money. You shouldn’t wait until the end of the month to see if anything is left to save. This is the approach that ordinary people take, and it will never lead you to financial freedom.

The Financial Map for Managing Money

Managing your money well

L’implementazione di un budget personale efficace non è solo una buona abitudine ma un passo cruciale verso la realizzazione dei tuoi obiettivi di indipendenza finanziaria che ti permetterà di prendere il controllo delle tue finanze.

A budget gives you a clear view of your income and expenses, helping you manage your money better and avoid spending more than you earn. This situation is much more common than you might imagine—most people don’t have control over their finances.

With a properly created personal budget, you can strategically plan to save for specific goals beyond achieving financial independence. For example, buying a house or saving for your children’s education, ensuring you allocate enough funds to reach these milestones. You increase the likelihood of achieving your goals.

Implementing an effective personal budget isn’t just a good habit, but a crucial step toward realizing your financial independence goals, which will allow you to take control of your finances

Discipline and the Personal Budget

Sticking to a budget requires discipline and constant commitment, but the long-term benefits are immeasurable. It helps you establish healthy financial priorities, reduce money-related stress, and, most importantly, build a secure future.

Finance is easy to understand but difficult to execute

In our next article, we’ll explore the third step: Execution, which is the hardest part.

On avance!