Optimizing savings provides multiple benefits. For example, do you think that by stopping your daily coffee habit at the bar you could become a millionaire? The answer to this question might surprise you.

I’ve already introduced the model I’ve used for years to manage my finances. Now it’s time to go into more detail, starting with tracking all your expenses. This process is called: Actual.

The System for Recording Expenses

To get a general overview of your financial situation and, most importantly, meaningful data, you need at least 12 months of recorded expenses. Over the course of a year, various events, unexpected expenses, holidays, etc., will occur. In the end, you will have gathered average data that will be extremely useful.

This tedious activity can be done in parallel with other actions. Your first year’s budget will likely be somewhat rough, and the actions you take will be more general. Over time, you’ll refine the figures and your report.

The most important thing is to start the project and begin recording all income and expenses.

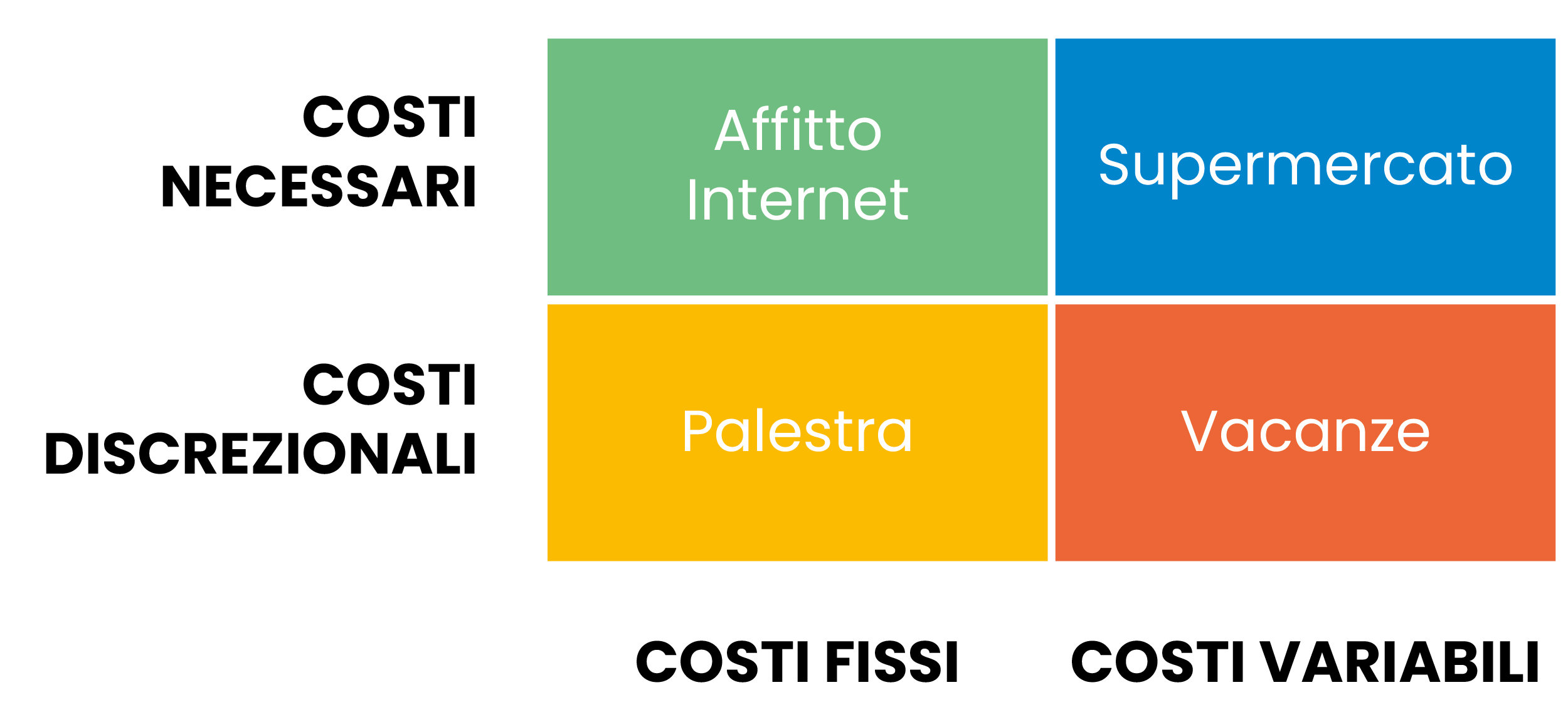

To correctly track costs, I’ve created a simple cost matrix. In this matrix, I’ve separated fixed costs from variable ones and necessary costs from discretionary ones. It’s essential to understand the nature of different costs to conduct a thorough analysis and implement effective action. Here’s an example—naturally customizable to your needs—of how I’ve allocated all my costs:

The Cost Matrix

The main rule is that the matrix must contain every cost. Don’t forget that we are still talking about personal finance, so there is no one-size-fits-all rule. For example, for me, the internet is a fixed and necessary cost due to the type of work I do, so I can’t do without it; maybe for you, it’s different. On the other hand, I consider going to the gym discretionary because I can just go for a run, so I can cut that cost if I need to stick to my budget.

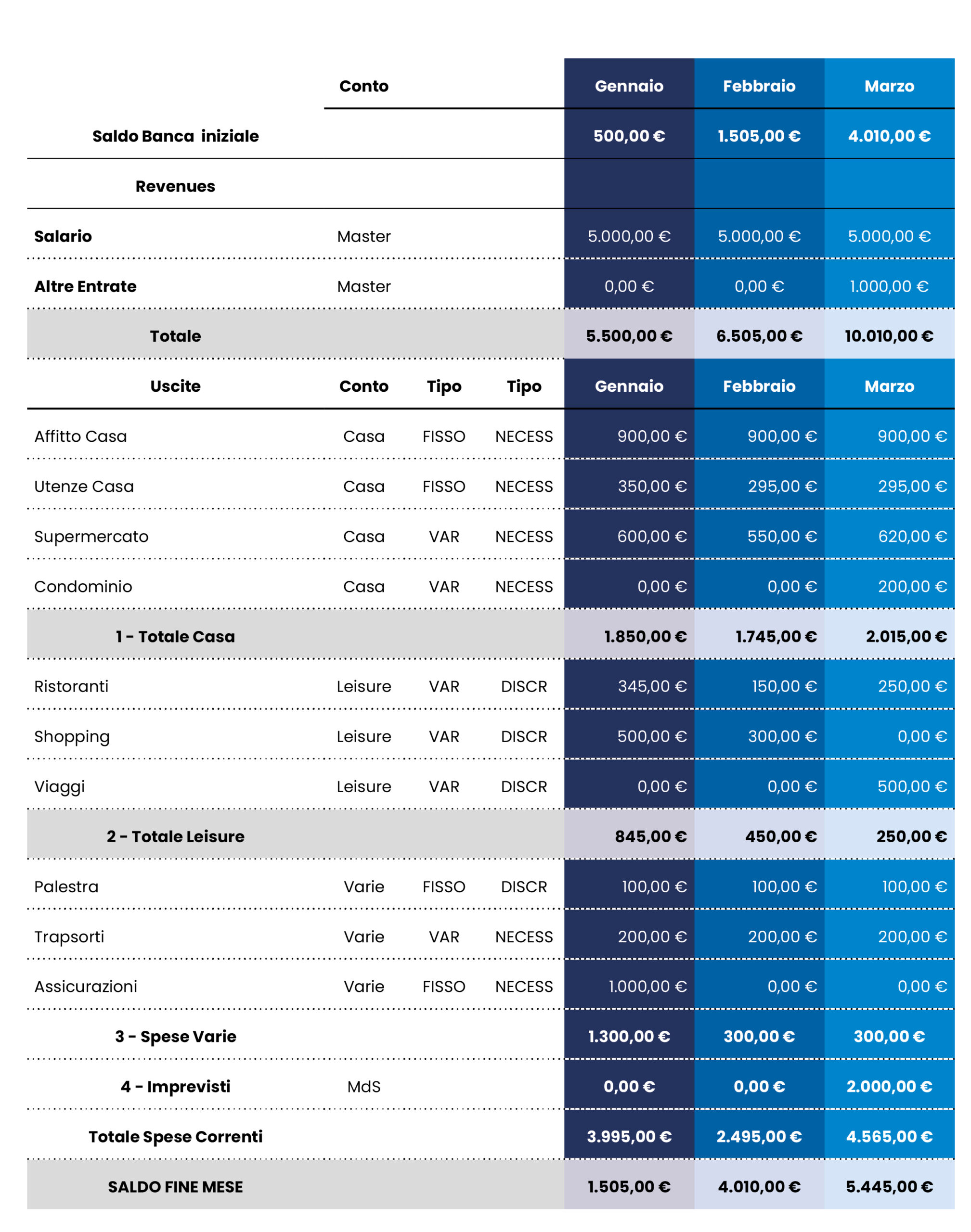

Now that we’ve clarified the meaning of the cost matrix, here’s an example of how my spreadsheet is structured:

In the various columns, you’ll find the description of the activity to be recorded, the type of account to allocate it to, the nature of the cost, and the months in which the transactions are recorded.

Income

Income consists of the money generated from work, which we aim to increase by strengthening Human Capital, along with any other income streams such as rental payments. Don’t forget to start with the total balance of your bank accounts on the first of every month.

This process takes time, but it is key to achieving financial independence. Income is the most powerful weapon you have to optimize savings, and it can grow exponentially, while costs can only be reduced to a certain point.

Expenses

Expenses represent the costs incurred and can be recorded using different criteria, such as separating fixed costs from variable ones and necessary costs from discretionary ones. As you saw at the beginning of this article, I used a matrix to track expenses, categorizing each one into one of the four quadrants. Allocating some costs between necessary and discretionary is very personal and depends on your priorities.

My advice is to approach the task in two steps. Initially, record everything in detail and then group the cost items into different categories that should be representative and account for at least 5% or 10% of your total expenses. You can use filters in Excel. Analyzing the data from the first few months, you’ll probably be surprised to see how much you’ve spent on certain activities like shopping and how small, percentage-wise, the portion dedicated to savings is.

Questions to Ask Yourself to Optimize Savings

The first question to ask yourself is: are all these expenses truly necessary, or are there areas where you could cut back? Of course, there will be room for adjustments, otherwise, you wouldn’t be reading my blog.

Next, you should ask yourself which of these expenses are essential because they contribute to your well-being. This is a sensitive issue, so always use common sense.

Personally, I believe there always needs to be a balance. Frugality is fine, but only to a certain extent. We’re still social animals, so keep having your coffee at the bar, because, despite what some personal finance “gurus” might say, I assure you that you will never become a millionaire by saving one euro a day on coffee. If you enjoy dining out, keep going, perhaps reducing the frequency or being more mindful of the wine you choose.

The most important thing:

Work with an 80/20 Approach

Pareto’s rule is a statistical method encountered in many complex cause-and-effect systems. In practice, it tells us that 20% of the causes generate 80% of the effects. You need to focus on that 20%. The game is played with the larger figures that often require negotiation, such as the rent contract, car payments, mortgage rates, or insurance policies. Often, it’s a few important choices that make the difference in your ability to save; that’s why financial literacy is so important.

This deep dive into personal expense management highlights the importance of a conscious allocation of financial resources.

The Key Point for Optimizing Savings

We’ve seen how a careful analysis of expenses can not only give you a clear view of your spending habits but also open opportunities to optimize savings and thus move closer to financial freedom.

Applying Pareto’s rule to personal finance management can be an effective strategy, focusing efforts on the areas that have the greatest impact on your financial situation but are also the most challenging to manage.

As you move forward in this journey, I encourage you to find a balance between frugality and enjoying life, remembering that the wisest financial choices are those that support your long-term goals without compromising your daily happiness. That’s the key: finding the right balance to optimize savings, even if it’s not always easy.

On avance!