Investment management fees are something that, if not carefully monitored, can turn into a significant financial drain. Have you ever thought about paying forty times more for a coffee? It may seem like hyperbole, but in this article, we’ll see that this happens much more often than you might imagine.

Passive management increases our chances of success. Naturally, we cannot eliminate systemic risk, which is intrinsic to financial markets. As investors, we must accept it, and at best, we can measure it through volatility. My approach, both in life and investing, is to focus on what I can control: costs. Passive management, unlike active management, has very low costs and is extremely efficient from a tax perspective.

Basis Points in Management Costs

Before presenting the numbers, I believe it’s important to understand the correct order of magnitude. One basis point is equal to 0.01%, while 10 basis points correspond to 0.10%, and one hundred basis points to 1%. What might seem like a small percentage discrepancy can, over the long term, turn into hundreds of thousands of euros in missed gains. I assure you that these differences matter in terms of capital growth and achieving financial independence.

My portfolio consists of three ETFs, with a Total Expense Ratio (TER) of 15 basis points, equivalent to 0.15%. According to my investment principles, a portfolio should never have a TER higher than 30 basis points.

A passive management ETF, which replicates the S&P 500, costs less than ten basis points. For example, the one in my portfolio costs 0.07%. Additionally, it is tax-efficient, highly transparent, liquid on the markets, and has no entry or exit fees. The only thing you may have to pay is the broker with whom you purchase the instrument. If the index has returned 10%, the ETF will return 9.93%. The difference is due to the TER, which in my case is seven basis points. In some cases, efficient ETF management in rebalancing and/or reinvesting dividends, thanks to increasingly powerful and precise software, can even eliminate or limit the gap caused by management costs.

Investment Funds Sold by Banks

In contrast, a classic equity fund offered by your bank, which essentially does the same thing but without all the advantages of an ETF, is definitely less transparent and is not traded on the stock exchange. It will cost, including all applied fees (which could be the subject of another book), at least between 2% and 3%, equivalent to 300 basis points.

The question is: why pay 42 times more for a coffee? (300/7). I wonder, €42 for a coffee that costs €1? It’s likely that the more expensive coffee is also of lower quality.

Do you remember that I mentioned earlier that actively managed funds generally do not outperform the index? They perform worse than your ETF and cost up to 42 times more.

The Comparison of Management Costs

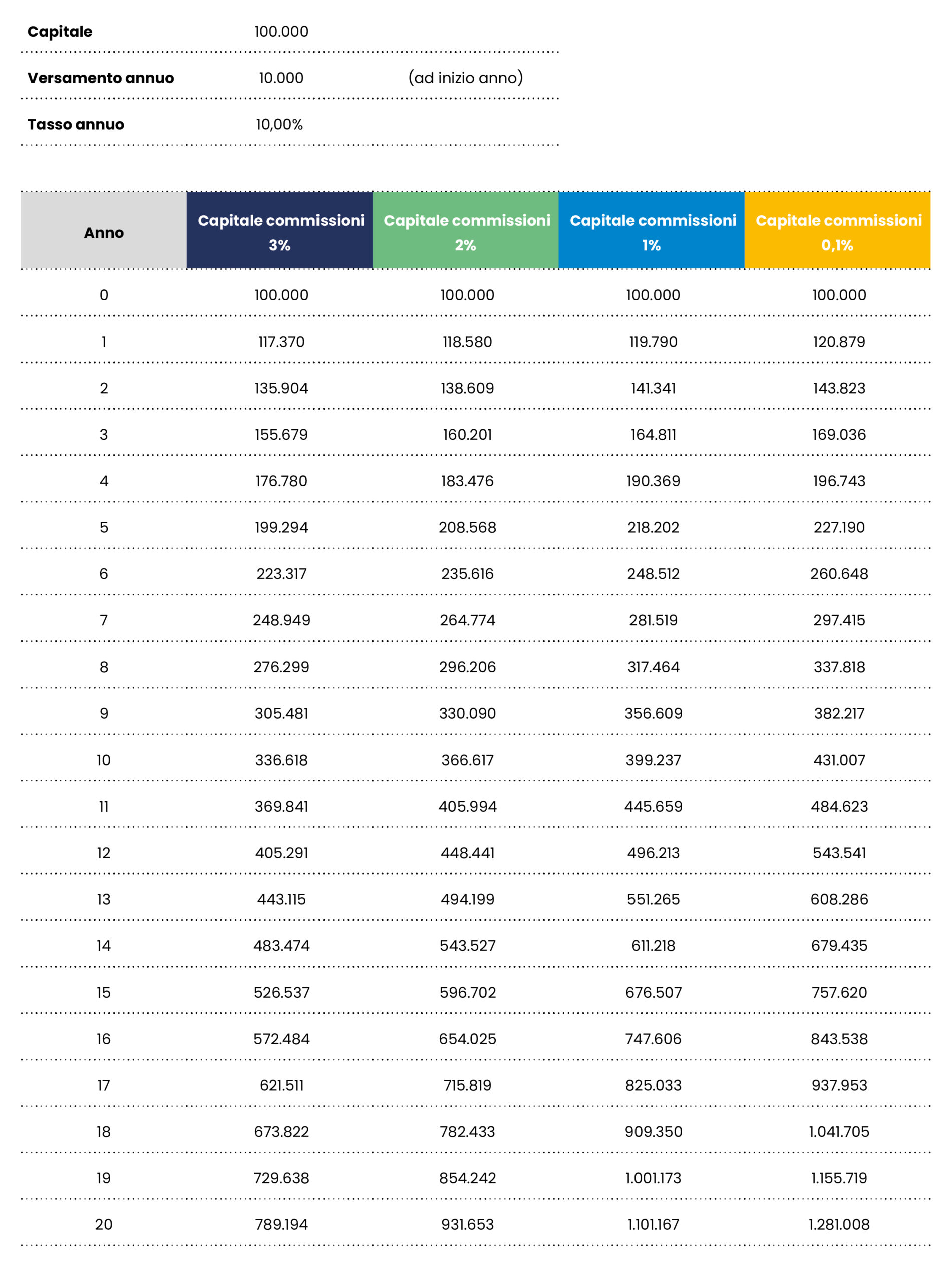

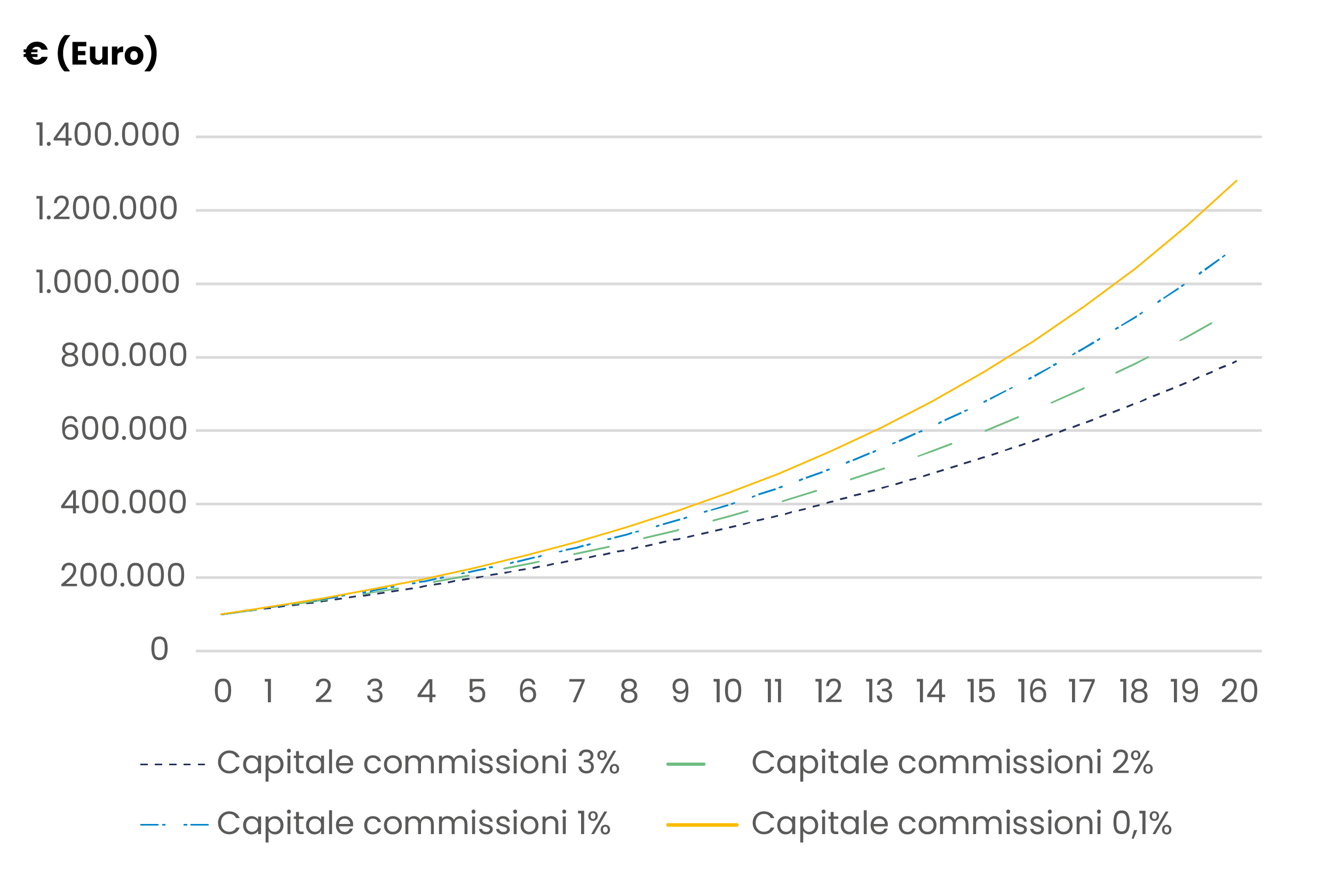

Once again, the numbers never lie, and I believe a chart can vividly illustrate the concept. Let’s imagine the same assumptions as the previous example on compound interest and add only the fees applied by banks.

Let’s imagine four levels of different fees: the first scenario is represented by our passive ETF, costing 0.07%. The other three are funds or hybrid ETFs, with fees ranging from 1% to 3%, depending on how “trendy” the financial products are.

Impact of fees in the long term.

It is clear that the game is played on fees, so I encourage you to pay close attention to this aspect when it comes to investing.

The results speak for themselves. Over twenty years, those few percentage points have turned into hundreds of thousands of euros, specifically 492,000€ in the case of a 3% fee. Measure this in terms of opportunity cost and the number of years of work required to achieve financial independence.

All the Elements for Investing with ETFs

To recap, in the previous articles, we have explored several fundamental aspects of successful ETF investing.

We analyzed the differences between active and passive management, emphasizing how passive management, through the use of ETFs, increases the chances of long-term success. Scientific research has shown that markets are extremely efficient and that it is very difficult to outperform them.

We delved into criteria for selecting ETFs, focusing on three key elements: the use of profits, the fund size, and the replication method. Choosing accumulation ETFs allows you to make the most of compound interest.

We discussed the importance of management costs, highlighting how small differences in costs can have a significant impact on long-term returns. Passive management ETFs tend to have much lower costs compared to active funds, allowing investors to keep a larger portion of their gains.

Passive management, attention to management costs, and careful ETF selection are fundamental elements for building a successful portfolio.

By following these guidelines, you as an investor can increase your chances of achieving financial independence and achieving sustainable capital growth.

On avance!