.

New strategies and ideas to improve how you save. The time has finally come to take action. Naturally, as with all activities, execution will be the most challenging part.

Strategy is a commodity, execution is an art

Peter Drucker

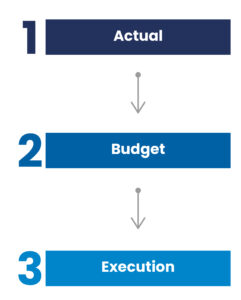

Before we begin, I think it’s useful to briefly recap the model I use to manage my finances. The plan consists of three phases:

- ACTUAL, tracking expenses to get a snapshot of your current situation;

- BUDGET, defining a personal budget based on the data obtained;

- EXECUTION, taking action.

For simplicity, it can also be represented by the following diagram:

The first thing you need to work on is triggering a new habit in your brain.

Small habits create big changes

Write Down Your Goals

It’s very helpful to always write down your goals, as they become motivating when they are achieved. For this reason, I always start new challenges with small goals that need to be met, and then continue raising the bar.

You need to try to trigger the snowball effect. With this method, I’ve achieved results that were initially unimaginable for me, even in areas beyond finance.

Moving on to more practical aspects, when analyzing the data, it’s likely that some out-of-control expenses will emerge. Imagine, for example, that you or your spouse spend half your salary on shopping. You’ll need to work on solving the problem.

In the article Your True Compensation: Strategies to Increase Savings, we explored a different metric to assign the right value to things.

Strategies to Avoid Compulsive Shopping

In the example just described, one initial action to take could be using more cash and fewer credit cards. It’s widely proven that using cash reduces spending—think about how pulling out banknotes from your wallet feels more “painful” than swiping a card.

Today, with contactless cards, everything is faster and easier. Use these new tools with great care. I realize that in modern society, living without credit cards is almost impossible, but you need to learn how to use them consciously and find a balance between the two methods.

In the budget phase, you’ll have already set the amount allocated to shopping; reloading the card, that amount must last for the entire month. In the past, people used envelopes or jars, but I use different reloadable cards for various spending categories, which I fund monthly or annually depending on the activity. My favorite is Revolut, which I fund with transfers based on my personal budget.

I won’t hide that I made a few planning mistakes at first and found myself temporarily “in the red”; it was an embarrassing situation, but luckily everything was resolved later.

If your issue is online shopping, the cash rule doesn’t apply. In this case, try to avoid making impulsive purchases. Controlling your impulses and staying calm in finance is a fundamental rule for success. I suggest a small trick: I put items in the e-commerce cart and confirm the purchase the next day. Sometimes, after reflecting with a cool head, I realize that some items aren’t that important or urgent, and the purchase can be postponed to the following months or until my budget allows.

The Power of Analysis

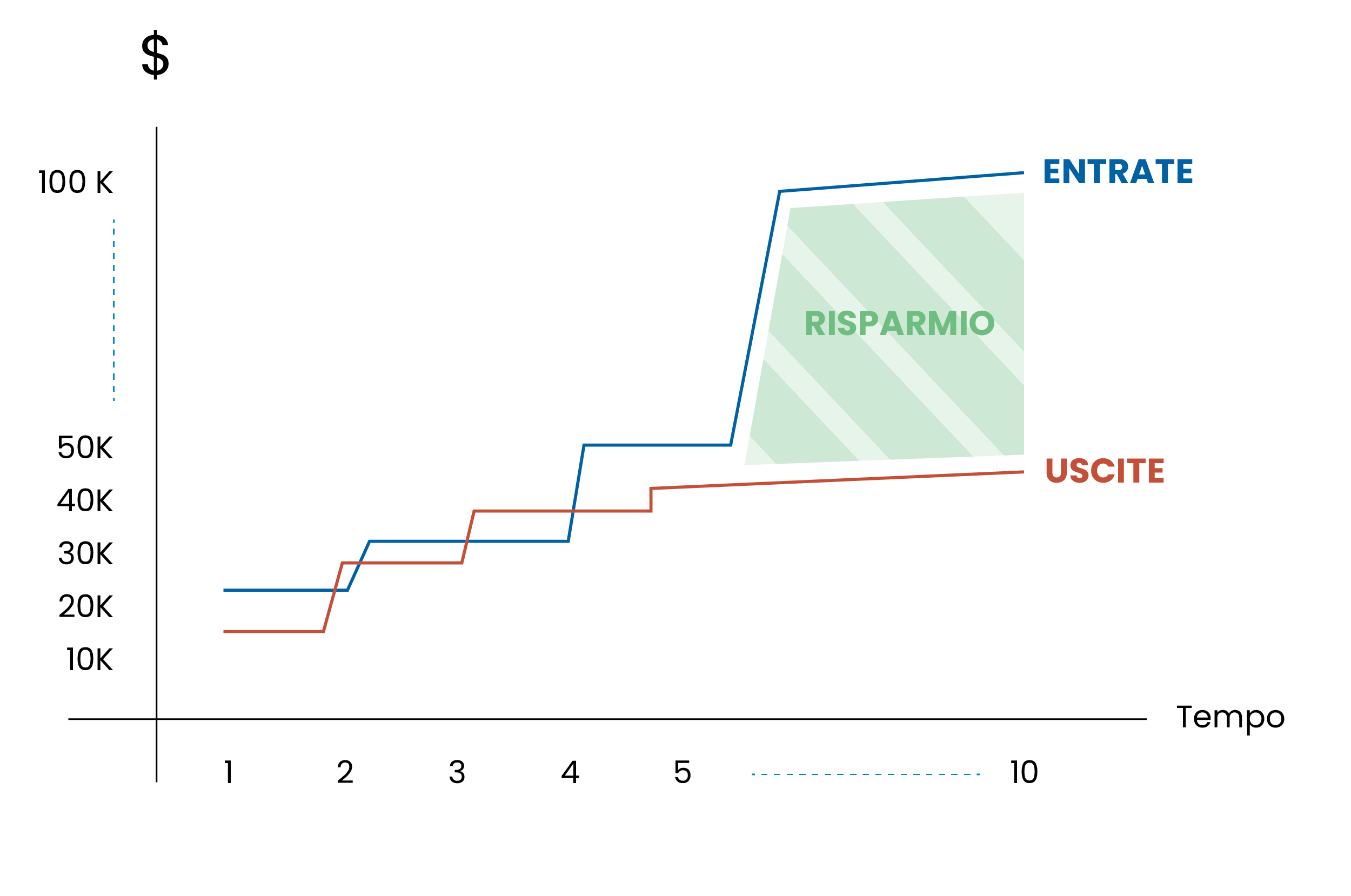

In general, the more analytical you are, the more effective your actions will be, and the faster the results. Initially, I recommend updating your spreadsheet with the “budget” and “actual” columns on a monthly basis, printing it out, and displaying it with a chart. Visualizing the results, seeing expenses decrease and savings increase, is highly motivating.

Savings Flow

Remember, your savings goals and spending limits were previously set during the budget phase. Discipline and patience are the two virtues needed to carry out this activity. During the first year, track everything monthly until you internalize the process. In the end, this task can take about 15 minutes each week, so it’s not a big commitment. I’ve been doing it every Sunday morning since 2015, and by now it’s such a well-established habit that I can’t live without it.

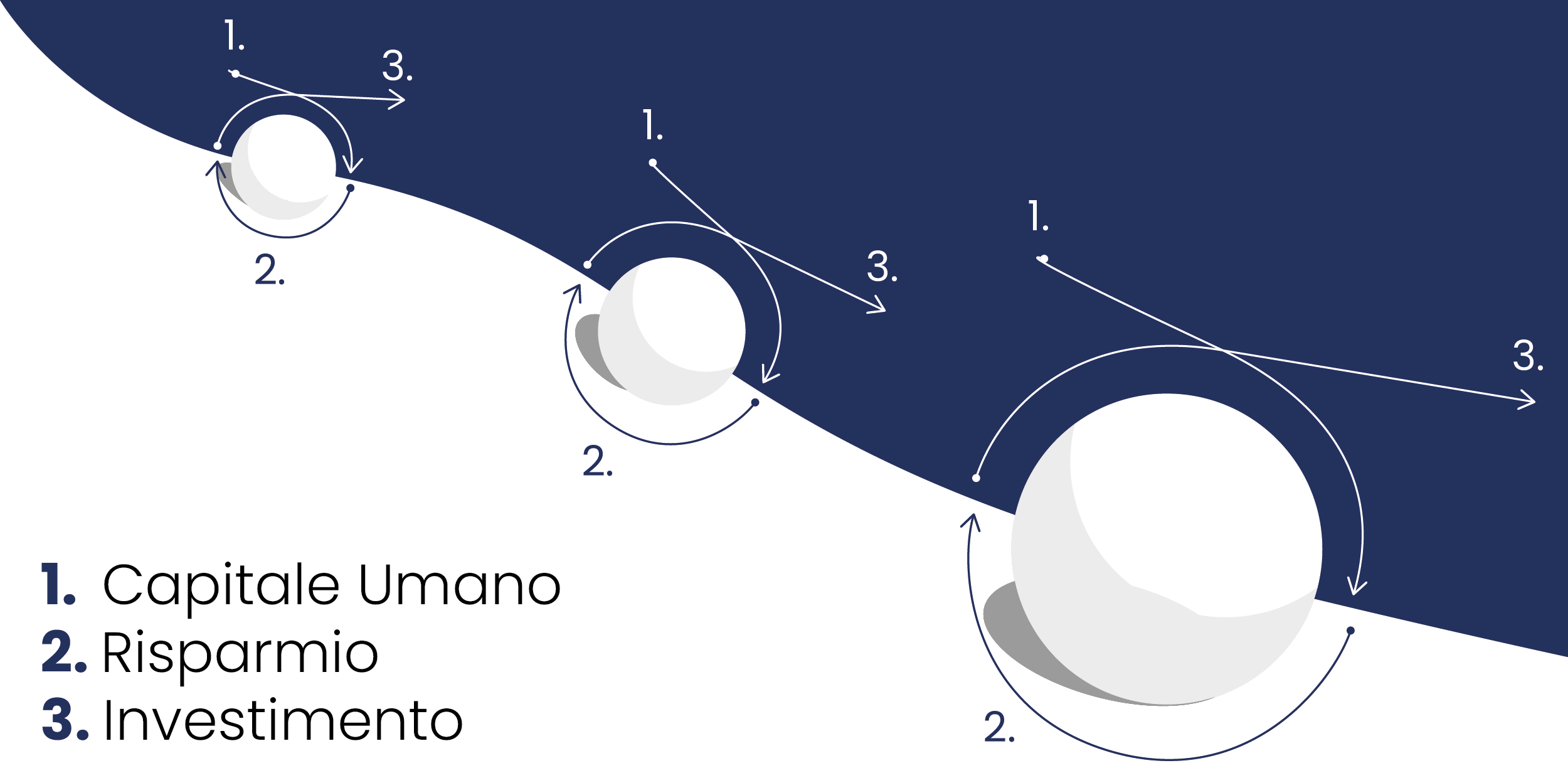

In my reference model, the goal of Step 2, represented by the Savings section, is to learn how to manage the money you earn using techniques that aren’t taught in school but have produced excellent results for many people. This will allow you to naturally increase your savings rate and prepare you to start investing in the Investments section (Step 3); doing it earlier might have been premature.

The Three Phases to Achieve Financial Independence

Don’t forget that it’s crucial, to increase your chances of success, to map out a clear path and always write down your goals to visualize them in your mind and turn them into a habit

Executing the Strategies

In conclusion, executing your personal budget is a crucial step toward achieving your financial goals.

Implementing strategies and a well-structured plan requires discipline and consistency, but the benefits are significant and long-lasting.

By implementing strategies to control and reduce expenses, you’ll not only save more, but you’ll also live with greater peace of mind, knowing that you’re building a solid financial future. With each small goal achieved, your confidence will grow, and with it, your ability to tackle even bigger financial challenges.

Success in money management doesn’t just come from accumulating resources but also from the ability to manage them wisely to achieve your dreams and improve your quality of life.

On avance!